Finance Minister Joe Oliver delivered his first Federal budget on April 21st, 2015.

Finance Minister Joe Oliver delivered his first Federal budget on April 21st, 2015.

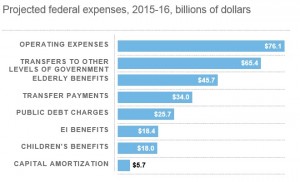

While you’ve probably seen plenty of media coverage, I thought you would appreciate an overview of how some of the budget items that relate to investments and taxes.

Increase TFSA contribution limit from $5,500 to $10,000

The proposed change is retroactive to January 1, 2015. For Canadians who are over age 18 and have not contributed since the TFSA’s creation in 2009, you now have $41,000 in contribution room.

Lower minimum RRIF withdrawals from 7.38% to 5.28%

The proposed changes to RRIF rules will mean seniors won’t have to withdraw as much money from their retirement savings. Required withdrawal rates still increase every year, but instead of topping out at 20% at age 94, the cap isn’t reached until age 95. The change is meant to reduce the risk of seniors outliving their savings. However, it could lead to a higher tax liability upon death if you leave too much money inside your RRIFs.

Introduce new Home Accessibility Tax Credit

Another budget item aimed at seniors and others who qualify for the Disability Tax Credit is a new Home Accessibility Tax Credit. This 15% non-refundable tax credit applies to up to $10,000 of renovations, such as wheelchair ramps, walk-in bathtubs and wheel-in showers.

Reduce Small Business Tax Rate from 11% to 9%

Small businesses will get to keep more of their earnings. This year’s budget proposes to reduce the small business tax rate to 9% by 2019 – or 2% over the next four years. The reduction generally applies to the first $500,000 of business income. There is a corresponding change to the Dividend Tax Credit from 11% to 9%, and gross-up factor from 18% to 15%, by 2019. Small business owners also will get a tax break if they sell their companies and donate the private company shares to charity. To be eligible, a sale must take place in 2017 or later.

Overall

With proper planning, people who are in higher tax brackets, own businesses or are nearing retirement will benefit from changes in this federal budget.

Thoughts

For those in lower tax brackets, TFSAs can become more advantageous than RRSPs. Those who are nearing retirement can take advantage of early RRIF withdrawal benefits and then move the money into a TFSA and keep it sheltered. Or, if you’ve already contributed the old $36,500 maximum, you could now move some non-registered investments into TFSAs.

In cases where large capital gains might apply, this might not be a strategy worth pursuing. We can talk about whether this strategy is a good idea when we meet.

I trust that you find these highlights useful. If you’d like to discuss these and other Federal budget initiatives and how they affect your financial plan, please don’t hesitate to contact me.

Remember to always “Dream It. Plan It. Live It.”

I am here to help you on your journey. Reach out if I can be of any assistance.